In the previous post, I laid out a truth that tends to land with a dull thud rather than a dramatic crash: there are only three possible retirement outcomes. No matter how complex the strategy, how clever the product, or how confident the forecast, every retirement ends up in one of three places.

This article is about the first—and most problematic—of those outcomes: running out of money before you run out of life.

It’s the outcome no one plans for.

It’s the outcome most people assume will happen to someone else.

And it’s an outcome that emerges quietly, when the basic variables of retirement are misaligned for too long.

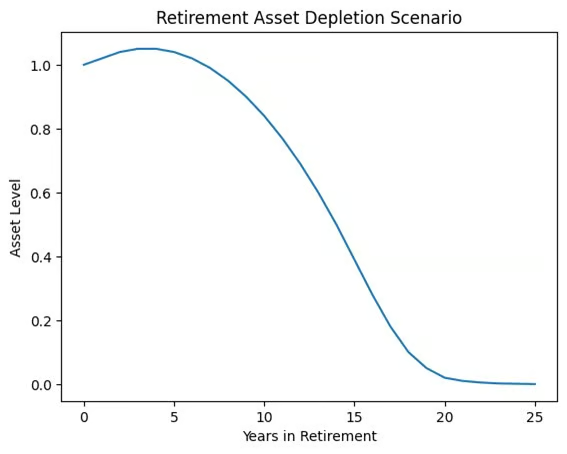

What makes this outcome especially cruel is that it rarely announces itself early. It doesn’t arrive with sirens. It arrives gradually, almost politely, disguised as “probably fine.”

In the early years of retirement, things often look stable. Income arrives. Expenses are manageable. Markets may cooperate for a while. Withdrawals don’t feel aggressive. In fact, retirees often spend less at first, still carrying the habits of accumulation.

But beneath that calm surface, lifestyle inflation and actual inflation are both at work. Healthcare costs inch upward. Insurance premiums rise. Travel becomes more expensive. Taxes behave differently than expected. And slowly, the amount needed to maintain a basic quality of life begins to exceed what the portfolio reliably produces.

At first, the retiree dips into principal just a little. It doesn’t feel dangerous. After all, the portfolio is there to be used.

But over time, those small withdrawals from principal compound in the wrong direction. The portfolio shrinks. Future income capacity shrinks with it. And the gap between spending needs and portfolio returns widens.

That’s when the clock becomes impossible to ignore.

This outcome almost always begins years—even decades—earlier, with saving decisions that felt reasonable in the moment. Many people save what they can while juggling careers, kids, mortgages, student loans, and aging parents. Life is full, and retirement feels distant.

“I’ll save more later” is not laziness. It’s optimism. It’s faith in future capacity.

The problem is that retirement math doesn’t reward good intentions. If savings rates remain too low for too long, the portfolio never reaches the size required to support decades of inflation-adjusted withdrawals. And once time is gone, no amount of market performance can fully replace it.

I’ve watched people rely on assumptions that didn’t hold—Social Security estimates that changed, pensions that disappeared, overly aggressive market expectations, careers that ended earlier than planned. When saving is postponed, the opportunity for compounding quietly evaporates. What’s left is a smaller engine trying to power a long journey.

Then there is the most misunderstood variable of all: equity ownership.

For much of my career, I’ve pushed back against the idea that equities are inherently dangerous in retirement. Unfortunately, other than the few people I call “clients,” I have barely made an impact amidst all the catastrophist noise.

The belief that equities are risky is rooted in short-term thinking. It focuses on volatility while ignoring inflation—the most persistent risk retirees face.

Equities are not “the market.” They are ownership in the great businesses of the United States and the world. They represent people solving problems, building tools, delivering healthcare, producing energy, feeding families, and adapting—again and again—to always unpredictable, ever-changing conditions.

In my Gathering Darkness teachings, I return to this idea repeatedly: when the world feels uncertain, ownership in human ingenuity and productivity has historically been the most reliable long-term hedge against that uncertainty.

The real risk for investors is not owning too many equities. It’s owning too few. When retirees dramatically reduce equity exposure at retirement, they often lock themselves into returns that cannot outpace inflation over a 20- or 30-year horizon. “Fixed” income in a rising-cost world is financial suicide.

The portfolio may feel stable year to year, but purchasing power erodes quietly in the background. Income looks predictable… until it isn’t enough.

At the same time, equity ownership without planning and preparation can create its own problems. Markets will decline. Sometimes sharply. Almost always unexpectedly. The danger isn’t volatility itself; it’s being forced to sell during volatility.

This is why maintaining a meaningful emergency fund—or what I often call a volatility buffer—is essential. Cash is not there to generate returns. It’s there to buy time. It allows retirees to continue spending during severe market drawdowns without liquidating equities at depressed prices. It turns market declines from existential threats into temporary discomforts.

Without that buffer (and perhaps a smidge of spending flexibility), even a well-constructed portfolio can be undermined by bad timing.

Finally, there is the withdrawal rate—the most personal and emotionally charged variable of all.

When spending consistently exceeds what a portfolio can sustainably support, the outcome is inevitable. Inflation ensures that a small mismatch becomes a large one over time. Principal depletion accelerates. Future income shrinks. Options narrow.

What makes this so hard is that spending isn’t abstract. It represents identity, freedom, generosity, dignity, and long-deferred joy. Cutting back doesn’t feel like an adjustment; it feels like a loss.

I’ve seen retirees cling to withdrawal rates that made sense once, refusing to revisit them as circumstances changed. I’ve also seen people spend aggressively early in retirement because “these are the good years,” only to discover that longevity is both a gift and a multiplier of financial risk.

Running out of money is not just a financial failure. It’s an emotional one. It shows up as anxiety, shame, and fear of becoming a burden. It strains relationships. It limits choices. It turns retirement into something to endure rather than inhabit.

And yet, this outcome is not inevitable.

It happens when saving, equity ownership, and spending are left on autopilot. It happens when plans are built on hope instead of humility. It happens when we assume tomorrow will fix what today avoids.

Awareness changes behavior.

Behavior changes outcomes.

Next, I’ll turn to the second retirement outcome—the one most prepared retirees experience. It’s the place where spending and returns find balance, where portfolios fluctuate but endure, and where flexibility becomes the defining skill.

I call it orbit. And understanding how to stay there may be the difference between fear and freedom.