(Part Three of a Four-Part Series on the Only Three Retirement Outcomes)

In the first article of this series, I described the only three retirement outcomes that exist. In the second, I explored the most painful of them—running out of money before you run out of life, a failure born not of bad luck but of misaligned decisions around saving, equity ownership, and spending.

This article is about the second outcome.

It’s the one most successful retirements occupy.

It’s the one that works most of the time.

And it’s the one that quietly demands the most humility.

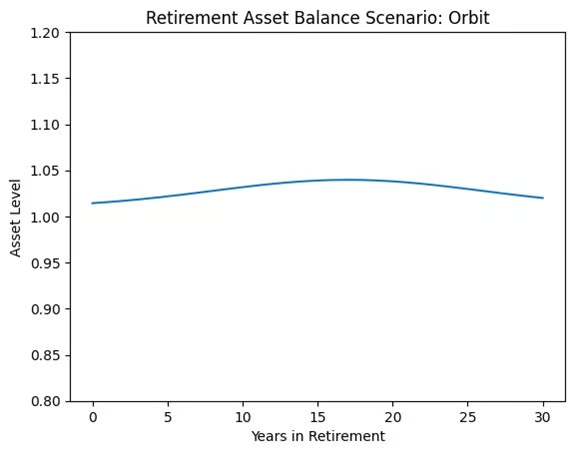

I call this outcome orbit.

Orbit is where a retiree’s inflation-adjusted spending and long-term portfolio returns find balance. Withdrawals are sustainable. The portfolio fluctuates, sometimes uncomfortably, but it largely holds its ground. Income supports life, and life respects the limits of income.

From the outside, orbit looks calm. Inside, it requires ongoing awareness.

This outcome is built during the accumulation years by steady saving—not necessarily heroic saving, but consistent saving. People who arrive in orbit may not have maximized every opportunity, but they showed up. They paid themselves first. They let compounding do its slow work.

By the time retirement begins, the portfolio is large enough to matter, but not so large that it overwhelms decision-making. The math works—but only if it’s treated with respect.

Equity ownership is central here, especially after retirement. Orbit is not achieved by abandoning equities. It’s achieved by owning a meaningful share of the great companies of the United States and the world—businesses that innovate, adapt, raise prices when costs rise, and compound value over time. This is not speculation. It is participation in global human progress.

When retirees own these businesses through broadly diversified equity funds, they give their portfolios a fighting chance to outpace inflation over long retirements. Without sufficient equity ownership, even a well-balanced plan slowly drifts towards the spending of principal. The portfolio may look stable year to year, but purchasing power quietly erodes. Income that once felt adequate begins to feel tight.

This is why, in my Gathering Darkness teachings, I return again and again to the idea that equity ownership is not a “growth” luxury—it is a long-term income survival asset. It’s how retirees stay connected to the real economy rather than trapped by nominal (read: fixed income) returns that lose ground over time.

Of course, equity ownership brings volatility. Markets will fall. Sometimes sharply. Sometimes without warning. In orbit, this is expected. It doesn’t need to be feared, but it demands respect.

The difference between staying in orbit and being knocked out of it often comes down to one unglamorous but essential decision: maintaining a meaningful cash reserve. A well-designed cash cushion allows retirees to continue spending during bear markets without selling equities at depressed prices. It buys patience. It turns volatility from a threat into something temporary and survivable.

Withdrawal discipline is the quiet backbone of this outcome. For decades, research has shown that a 4% withdrawal rate is a reasonable reference point for many retirees—a starting guide, not a guarantee and not a rule. It works best when paired with diversified equity ownership, flexibility in spending, and a willingness to adjust during difficult market periods.

Used thoughtfully, 4% provides structure to retirement income. It reminds retirees that sustainable income is a function of portfolio size, market behavior, and time. Yes, you can spend more if portfolios rise… but not too much more. And, there is no entitlement to continued high spending—if portfolios decline, spending may need to change as well. Those who remain flexible tend to fare best.

It’s also worth naming something clearly. In an orbit-style retirement, while income is sustained and life is well supported, the assets ultimately left behind for the next generation are often worth meaningfully less in real, inflation-adjusted terms than the assets at the start of retirement. The portfolio does its job—funding decades of living expenses—but it is not designed to grow dramatically beyond that. This is not a failure. It’s simply the tradeoff embedded in balance. Orbit delivers retirement income success, peace of mind, and dignity, with some legacy—just not a growing one.

For most people, this outcome is more than enough. It is a retirement-income success. It supports a full life—travel, generosity, time with family, and meaningful pursuits. It provides security without excess; comfort without complacency.

But for some retirees, that realization sparks a different question. Not “Will I be okay?” but “What becomes possible if my portfolio doesn’t merely endure?” What if disciplined saving, sustained equity ownership, and conservative withdrawals allow returns to exceed spending year after year? What if volatility no longer threatens lifestyle at all? What if the portfolio begins to grow again—not for consumption, but for contribution?

That question points beyond orbit.

Unchecked increases in spending, persistent inflation, or poorly managed risk can slowly pull a retiree inward toward failure. But careful planning, patience, and restraint can also push outward—toward a rarer outcome where the portfolio escapes gravity altogether.

Next week, I’ll explore the third and final retirement outcome.

It’s the one that feels almost mythical until you see it in practice.

It’s where portfolio returns consistently outpace spending.

It’s where unused returns compound forward.

It’s where volatility loses its power to threaten security.

I call it escape velocity.

And understanding how it works may fundamentally change how you think about what’s possible in retirement.